Gridwise blog

Tips, insights, and advice to help you earn more and work smarter, whether you do gig work, hourly, or shift work.

How to Make $1,000 a Week With Uber Eats in 2026 (Tips + Hourly Data)

In this blog, we'll explore the strategies and techniques that can show you how to earn $1000 per week as an Uber Eats delivery driver. We'll cover everything from optimizing your delivery zones and schedules to maximizing your tips and customer satisfaction. Whether you're a seasoned Uber Eats driver or just starting out, this guide will provide you with the insights and actionable steps to take your Uber Eats driver earnings to the next level.

Becoming an Uber Eats delivery partner can be a lucrative opportunity, especially if you're able to consistently earn $1000 a week. By understanding the platform, optimizing your delivery strategies, and focusing on customer satisfaction, you can maximize your earnings and turn Uber Eats into a reliable source of income.

We’ll cover the following topics to provide coaching and ideas to help you push your earnings up to that $1000 per week level:

[elementor-template id="20891"]

What do Uber Eats drivers do?

Uber Eats drivers deliver prepared food most of the time, but they also might shop for and deliver goods from convenience outlets and grocery stores. The job is pretty simple. You get a request for an order, you drive to the restaurant or store to pick it up, and then you deliver it to the customer. If you already drive for Uber, you can choose to take orders for Uber Eats delivery any time.

If you’re not an Uber Eats driver yet, it’s pretty easy to become one. This Gridwise post tells you what you need to do if you want to sign up and start making money Uber Eats style. Many rideshare drivers welcome the chance to deliver food rather than people. This article from Nerdwallet covers the Uber Eats gig from that angle.

There are some sweet advantages to working with Uber Eats. In lots of cities you don’t even need to have a car. You can use a bike or a scooter, or even walk, to make your rounds. If you do use a car, Uber Eats’ requirements are a lot easier to meet than they are for Uber rideshare driving.

You also have a lot of flexibility. You can shop and deliver convenience items and groceries, but you don’t have to. And, like most driving gigs, you can choose your own hours, and map out the locations where you want to work.

Use Gridwise features When to Drive and Where to Drive to help you figure out what work hours and which specific areas will be the most profitable for you. Real data from real delivery people will show you earning patterns for drivers in your town.

[elementor-template id="20949"]

How much can you earn doing Uber Eats?

The honest answer to this question is: basically, as much as you want! It all depends on how many hours you put in and how strategic you are about your gig. Earnings vary from one area to another, as this article from Entrepreneur points out. To give you a baseline, let’s look at the earnings of Uber Eats drivers who tracked their earnings with Gridwise.

Remember that these numbers show us only average earnings. To make $1,000 a week with Uber Eats, you’re going to have to be better than average, and we’ll show you how. For now, though, it’s good to have these figures so you get a ballpark number of where to start.

How much do Uber Eats drivers make?

Gridwise data tell us the following:

- Monthly earnings average around $444.00 per month.

- Gross earnings per trip are between $9.00 and $10.00.

- Tips make up about 50% of most Uber Eats drivers’ income, which amounts to about $225.00 per month.

Is Uber Eats good money? It can be. While there are other gigs that pay more per trip, if you drive for Uber Eats, you’ll always be pretty busy.

https://datawrapper.dwcdn.net/HPAz8/3

You can also see that, unlike many other gigs, tips play a huge role in Uber Eats earnings.

With these numbers as a baseline, what can we say about how to earn $1,000 a week with Uber Eats? As we said in the introduction, it’s going to be a hustle, but it’s really possible. To figure out how to make the most money with Uber Eats, let’s start by looking at how many trips these “average” drivers made each month.

We know that average gross earnings were $444.00 per month, and drivers got around $10.00 per trip. That means they took 44 or 45 trips per month, which breaks down to 11 trips per week. That’s not a lot of Uber Eats delivery, is it?

The fact that Uber Eats drivers averaged so few trips shows us that many drivers use more than one app at the same time. This is called multi-apping, and you can learn more about it in this Gridwise post. If you want to answer the question of how much you can make with Uber Eats, then you need to stick with the app and keep plugging away at those orders. You also need solid strategies, as well as some inside tips and tricks.

How to make the most money on Uber Eats: Delivery driving tactics

Getting to that $1,000 a week with Uber Eats isn’t so hard when you remember that the drivers we saw making about $111 a week were only taking around 11 trips in the same time period. That’s not much at all! If you work the Uber Eats app like a boss, you’ll soon have many more trips than that, easily reaching the number needed to get you to $1,000 a week. Now, let’s get to some tactics you’ll need to make that kind of bank.

- Stay with the Uber Eats app, and track your earnings. Gridwise can easily do that for you. Simply sync your Uber Eats app with Gridwise, and you’ll be able to see how much you’ve earned with Uber Eats, what times were most profitable, and your average hourly pay. Racking up trips with Uber Eats has other benefits, including perks and bonuses that are awarded to top drivers.

- Leverage surge pricing and promotions. Surge pricing is applied when there is a lot of demand. When surge pricing is in effect, many of the trips you make will pay more than usual. Promotions are offered to drivers who complete a given number of trips in a certain time period. High traffic volume days, nights, and times give you these chances to get extra earnings. Challenging yourself to complete the right number of trips for promotions will add to the number of trips you can count on for big bucks, too. Learn more about Uber Eats surge pay, boosts, and promotions in this Gridwise blog post.

- Say yes to doubling up on orders. With Uber Eats, you can get back-to-back orders or receive batched orders. Back-to-back orders happen when you receive a new request while you’re on the way to deliver an original order. The Uber Eats app routes these trips automatically, so you won’t be sent out of your way.

Batched orders are Uber Eats’ way of bundling together orders from either the same restaurant, or two nearby eating establishments. You get money—and trip count credit—for all the orders you complete, plus customer tips, without having to make a bunch of separate trips.

- Turn on the charm and get bigger tips. Being nice really is part of the Uber Eats driver’s job, and getting tips is one way people who drive for Uber Eats make money beyond their basic pay.. Bring along those extra napkins and condiments, use equipment that keeps food and drinks at the right temperatures and prevents spilling, and consider your customers’ needs. If you deliver groceries, be extra careful with delicate items such as bread and eggs.

And, most important, follow your customers’ directions, and stay in communication with them if you are going to be delayed, or if you have questions about their order. This Gridwise post will tell how to get bigger tips as a delivery driver.

- Use even more charm to keep your ratings high. As an Uber Eats driver, you will be rated by the restaurant or store where you pick up the orders as well as the customers who are waiting for the deliveries. This two-way rating system is designed to keep you on your toes, so Uber can keep people satisfied with your service. Don’t worry—you get to rate them, too.

There’s another reason why your rating as a driver is important. It not only keeps you in good standing with Uber; it helps you to qualify for the Uber Eats Pro incentive program. To learn more about Uber Eats Pro, and what it takes to earn perks such as preferred services, discounts, and deals, check out this Gridwise blog post.

Smart business moves that seal the deal

Now that you know how to gobble up the deliveries you need to make $1,000 a week with Uber Eats, it’s going to be a breeze to get there. Let’s make it even easier, with business moves that boost your earnings and shrink your expenses. If you use these, it will also be easy to say yes when people ask, “Can you make good money with Uber Eats?”

Minimize expenses. Avoid racking up big fast-food bills by bringing your own food and beverages. You might not think you’re hungry when you first start your Uber Eats run, but once the aroma of pepperoni pizza, premium cheeseburgers, and piping hot fries start wafting through your car, that might change. Bring a sandwich or other healthy food from home, and buy bottled water in bulk to save tons of cash compared to what it costs to buy single servings.

Maximize tax deductions. Another way to minimize your expenses is to maximize your tax deductions. Start by tracking mileage with Gridwise.

Gridwise App

Gridwise captures every deductible mile you drive, including the distance you cover between the trips your driving app records. Know what expenses you can deduct, and put them to work for you when tax time comes. Learn more about tax deduction strategies in the Gridwise Tax Guide for drivers.

Boost earnings with referrals

As an independent contractor, you’re probably looking for ways to make even more money than you can with Uber Eats. And most gig workers like you enjoy getting passive income. With Uber Eats, there’s a really easy way to do that—referrals!

All you need to do is find friends and encourage them to deliver for Uber Eats. If they make a certain number of deliveries within a specified time, you will get paid for doing nothing more than having them sign up under your referral code! Rates of pay vary by city, so check your Uber Eats app to find out what the current deal might be, and learn more about the referral program on the Uber Eats website.

Also remember: “friends” don’t have to be your best buds. Many delivery people carry cards with a QR code linking to their referral information, so just about anyone you encounter can join Uber Eats and boost your earnings. You could meet a source of passive income at the gas station, on social media, or at your high school reunion. The more you hustle, the more there is to gain, right?

Master the art of self-employment

As an Uber Eats driver, you’re an independent contractor. That means the company isn’t going to withhold your taxes, provide insurance, keep track of your earnings, or tell you about tax deductions. You’ll have to do all these things for yourself.

If you want to maximize your tax advantages, open an official business entity. You can incorporate (create a corporation) or you can work as a limited liability corporation (LLC). You can also work with a DBA (Doing Business As) arrangement, but the corporation or LLC will do a better job of protecting you from liability.

Establishing a corporation or LLC offers better tax advantages than being a sole proprietor. For instance, if you simply collect your earnings into your private account, you’ll be charged self-employment taxes in most states. And paying extra taxes is something we all want to avoid, within legal limits, as much as possible.

Every Uber Eats driver needs to learn about self-employment, and there are some great resources you can review. Check out the CareerOneStop website about self employment which will help explain the basics. You can also check with a professional tax accountant, or look other websites to learn more about actually creating a business.

Scope out your market

Look at the area around you to see where you’re likely to get the most deliveries. Where are all the restaurants? Where might people be more inclined to order deliveries? What hours do you want to drive? What activities might be going on around those times? Think about late-night and after-school times as well as breakfast, lunch, and dinner times.

Be realistic about the potential for your area and aware of new services opening up. For example, in New York, there is already a tab on the Uber Eats app that allows customers to order groceries. In our article about the best food delivery service to work for you’ll see that Uber Eats stacks up well against other delivery companies, mainly because of its potential for expanded opportunities for drivers to earn.

So, is Uber Eats good money? As we said, it isn’t an automatic guarantee that everyone will make $1,000 a week with Uber Eats. Trying out the suggestions we give you here, though, should put you on the right track! Go out there and start stacking up those orders and raking in some impressive earnings!

[elementor-template id="20936"]

Get more inside information on Uber Eats in these posts from the Gridwise blog:

- The delivery driver guide: Using the Uber Eats app

- Everything you need to know about driving for Uber Eats

- Uber Eats Pro: What drivers need to know

- Looking for a different gig, part-time or full time job? Check out the Gridwise Job board.

Uber Eats FAQ

How does the Uber Eats platform work for drivers?

Uber Eats is a food delivery service that connects customers with local restaurants and independent delivery partners. As an Uber Eats driver, you'll receive notifications of nearby delivery requests, which you can accept and complete. The platform provides flexibility, allowing you to work on your own schedule and earn money based on the number of deliveries you complete.

What are the requirements to become an Uber Eats delivery partner?

To become an Uber Eats delivery partner, you'll need to meet certain requirements, such as having a valid driver's license, a registered vehicle, and passing a background check.

How can I choose the right delivery zone to maximize my earnings?

Selecting the right delivery zone can significantly impact your earnings, as some areas may have higher demand and better-paying orders. It's important to research and identify the zones in your area that tend to have the most consistent and lucrative delivery opportunities.

How can I take advantage of peak delivery hours and surge pricing?

Understanding peak delivery hours, such as mealtimes and weekends, and taking advantage of surge pricing can boost your earnings. Be aware of when demand is highest in your area and adjust your schedule accordingly to capitalize on these peak periods.

What are some tips for maximizing tips and customer satisfaction?

Providing excellent customer service and going the extra mile to ensure a positive experience can lead to more tips and repeat business. Prioritize communication, timeliness, and attention to detail to keep your customers happy and satisfied.

How can I set realistic weekly goals to reach my $1000 target?

To make $1000 a week with Uber Eats, it's essential to set realistic weekly goals and track your earnings and expenses. Start by determining your target earnings and breaking it down into achievable daily or weekly goals. This will help you stay on track and make adjustments as needed.

What are some strategies for efficient route planning and navigation?

Effective route planning and navigation can save you time and fuel, allowing you to complete more deliveries. Utilize mapping apps and take advantage of features like real-time traffic updates and turn-by-turn directions to find the quickest routes.

How can I balance my Uber Eats deliveries with other commitments?

Develop a schedule that allows you to capitalize on peak delivery hours while still maintaining a healthy work-life balance. Consider using tools like calendar apps to plan your availability and track your hours to ensure you're maximizing your earning potential without sacrificing your personal life.

What are the key considerations for maintaining my vehicle as an Uber Eats driver?

Keeping your car clean and well-maintained is crucial for maximizing your Uber Eats earnings. Regularly scheduled oil changes, tire rotations, and other preventive maintenance can help extend the life of your vehicle and minimize downtime. Additionally, budgeting for vehicle-related expenses, such as fuel, insurance, and repairs, will ensure you're accounting for these costs and maximizing your net earnings.

What are the tax obligations and legal considerations for Uber Eats drivers?

As an Uber Eats delivery driver, it's essential to understand the tax obligations and legal considerations that come with being an independent contractor. This includes properly reporting your earnings, deducting eligible business expenses, and making quarterly estimated tax payments. Additionally, you'll need to ensure you have the appropriate insurance coverage, such as personal auto insurance and possibly commercial auto insurance, to protect yourself and your vehicle while on the road making deliveries.

The Gridwise Job Board: Find Your Ideal Job or Gig Work

Gridwise is an essential assistant app created by gig workers for gig workers. Our mission is to support those engaged in gig work in every way possible. We understand how challenging it can be to deal with income instability, a lack of benefits, and job insecurity that often comes with gig work. The Gridwise app tracks and organizes earnings and expenses, and offers a wide array of discounts, deals, and services that make the lives of independent contractors easier and more rewarding.

We firmly believe it’s possible to make a viable living and create a gig experience that offers flexible hours, variety, and excitement. With issues such as consistent earnings and job security in mind, Gridwise is proud to offer a centralized platform that shows you how to find gig work and secure reliable opportunities. We’re proud to introduce the Gridwise Job Board.

[elementor-template id="20891"]

The Gridwise Job Board: Key features

Because Gridwise is dedicated to serving the gig worker community, we’ve filled the Gridwise Job Board with useful features that won’t waste your precious time.

- Comprehensive listings. Find part-time, full-time, temporary, and per-task work. Drive or deliver with your vehicle, utilize an employer’s vehicle, or even find non-driving gig work.

- User-friendly interface. Find the jobs that are right for you with a tap of your screen.

- Verified opportunities. We vet the jobs before they are listed to ensure you’re getting high-quality job postings.

How to get more gig work, seasonal, part-time or full-time jobs with the Gridwise Job Board

Looking specifically for “gig work apps” or “gig jobs near me?” You’re in luck. Our filters and search functions send you directly to the listings you seek.

Here’s how it works.

- Access the Job Board via the Gridwise website.

- Search for jobs by type, location, and more.

- Select the job that interests you, and read all about it.

- Scroll through the description, and if it appeals to you, click “Apply for job.”

Many types of jobs are available. Adjust the search filter to see the full variety of opportunities that will let you cash in. Deliver food, set up catering, do rideshare driving, get paid for doing package delivery, and much more. You’ll find short-term gigs, long-term contracts, and part-time positions.

Perks of the Gridwise Job Board for gig workers

Gig workers who know how to make extra money will appreciate how the Gridwise Job Board lets you multiply your chances of bringing in big earnings. Here’s how:

- Increased stability. Use the Gridwise Job Board to find part-time or permanent jobs in addition to the part-time gigs you already have. Always keep a steady stream of earning opportunities flowing toward you.

- Flexibility and autonomy. Choose jobs that fit your schedule, work around other jobs and family duties, and still leave room for some fun in your life. Discover side hustles to supplement your full-time job, permanently or just for the season.

- Skill development. Find part-time work that lets you use a skill you already have, or try your hand at something new. It’s a smart way to develop a portfolio to showcase what you can do, or even to find permanent employment.

Get Gridwise and stay up to date on the Gridwise Job Board

Gig workers need plenty of information and assistance, and Gridwise is here to give it to you. Download the app and get essential features such as

- seamless earnings tracking

- mileage tracking

- expense recording, including notes

- low-cost and no-cost insurance benefits

- access to affordable medical, dental, vision, mental health, and alternative care

- professional services including legal and financial help

- deals and discounts

- weather, events, and traffic reports

- inside information on where and when to drive

[elementor-template id="20936"]

More to know about gig work:

5 Best Mileage Trackers For Gig Drivers

Many drivers ask, “Do I really need a mileage tracking app?” The answer is simple: only if you want to have an accurate count of all the miles you can legally deduct from your taxable income! You might think your rideshare or delivery driving app has got you covered. After all, they do quite a good job of logging the miles you drive while you’re on a trip or delivery. But, if you want to have the best app to track mileage for Uber, Lyft, Doordash, Instacart, or the other apps you may use, you need more. Why is that?

Without a separate tracker, you’re missing the miles you drive in between pings. Did you realize that all the miles you drive, from the moment you begin your shift until it’s over (as long as you don’t drive several miles on a break to hang with your friends), are tax deductible! That means you need something besides your driving app to keep an accurate count of your travels. Read this Gridwise post to see how important it is to keep track of every deductible mile.

You won’t be surprised to hear that there’s an app for tracking miles. In fact, there are several of them. Here, we’re going to tell you about five top mileage tracking apps, and help you figure out which one is best for you.

Before we get to the list and identify the best mileage tracker app, let’s clarify what exactly a mileage tracking app is. According to G2.com’s technology glossary, mileage tracking is done for the purpose of keeping a log of mileage that is either reimbursable or tax deductible.

And yes, of course you can track your miles simply by taking readings on your odometer. But are you really prepared to account for how many miles you drove for personal reasons and subtract them from the total to get your business mileage? Even if you can remember all that and do the arithmetic, if you want an accurate reading of the miles you drive for business, and can therefore deduct, a mileage tracking app will save you a lot of trouble and prevent you from making costly errors.

Plus, as a gig driver, you have specific needs when it comes to a mileage tracker. Ideally, you’d be able to handle mileage tracking and several other functions all in one app. It can be maddening enough to deal with driving apps, particularly if you’re an avid multi-apper. You would want your mileage tracker app to help you keep account of other aspects of your business, including income, expenses, and inside information about the art of gig driving.

Not all mileage apps are equal, to be sure! Let’s look at five of the best apps to track mileage and figure out which is the best app to track mileage with Uber and Lyft, or what mileage tracker app is best for DoorDash.

[elementor-template id="20891"]

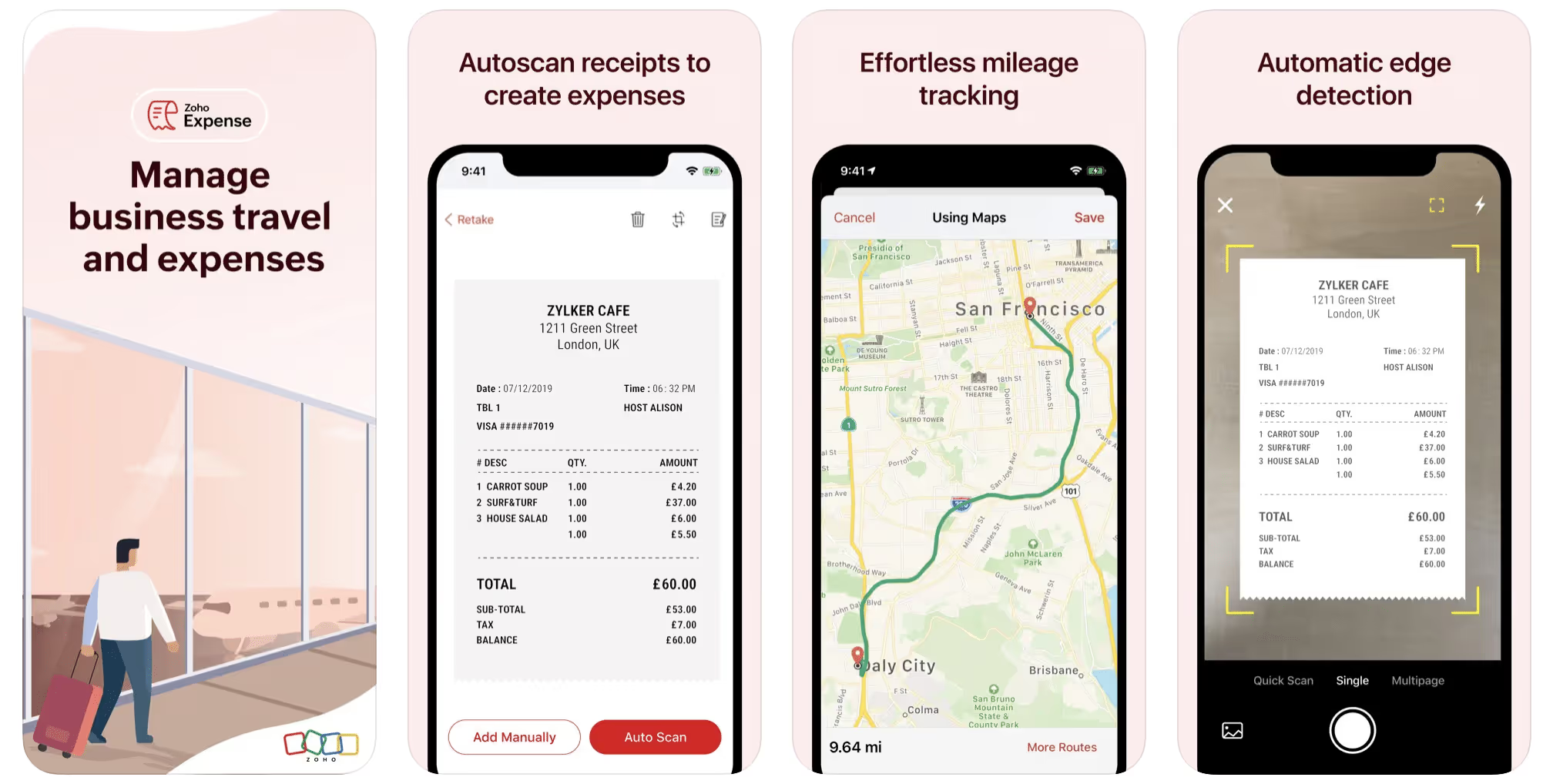

1. Zoho Expense

First up is Zoho Expense, which does exactly what its name says. This app is designed to allow companies to give employees a uniform way to create and submit expense reports. It can be used by individuals, including gig drivers, as well.

It includes a mileage tracker, as well as features that let you track other deductible expenses, including the ability to scan and record receipts.

Available on Android and Apple: Yes

Ratings: 4.8 stars on App Store, 4.7 stars on Google Play

Free Version: Yes

Subscription price: $3 per month, billed annually

Created specifically for gig drivers: No

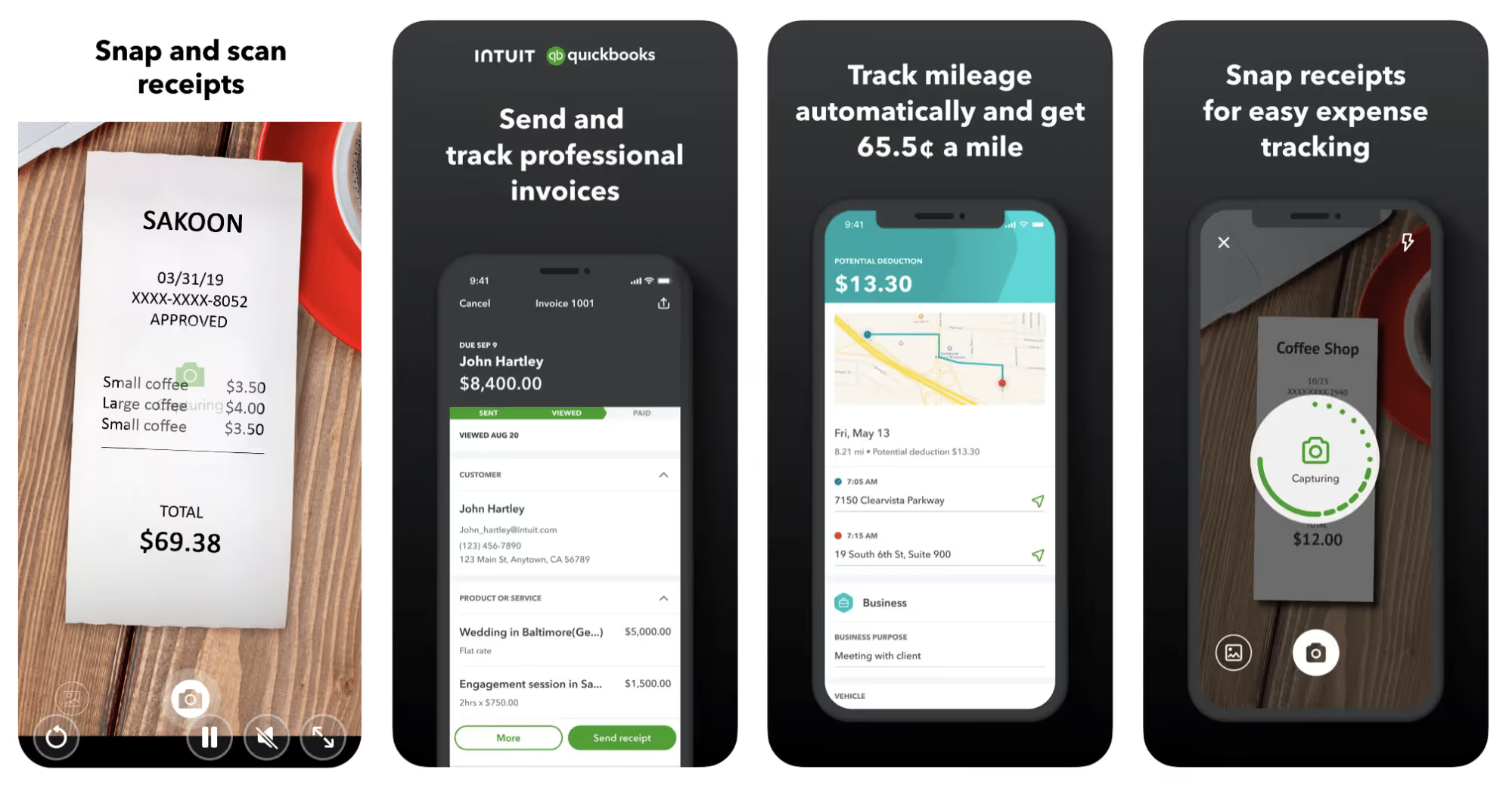

2. Quickbooks Online

Quickbooks Online is a cloud-based app that allows you to track your mileage, earnings, and expenses. The information you enter can then be used to generate various reports that prepare you for tax time. It also allows you to create graphs that illustrate your cash flow, and includes a receipt scanner so you can instantly record deductible expenses. Quickbooks is popular, highly reliable, and designed mainly to help people keep track of their small businesses.

Available on Android and Apple: Yes

Ratings: 4.7 stars on App Store, 4.4 stars on Google Play

Free version: 30-day free trial

Subscription price: $15 per month for basic version if purchased for 3 months or more

Created specifically for gig drivers: No

Source: quickbooks.intuit.com

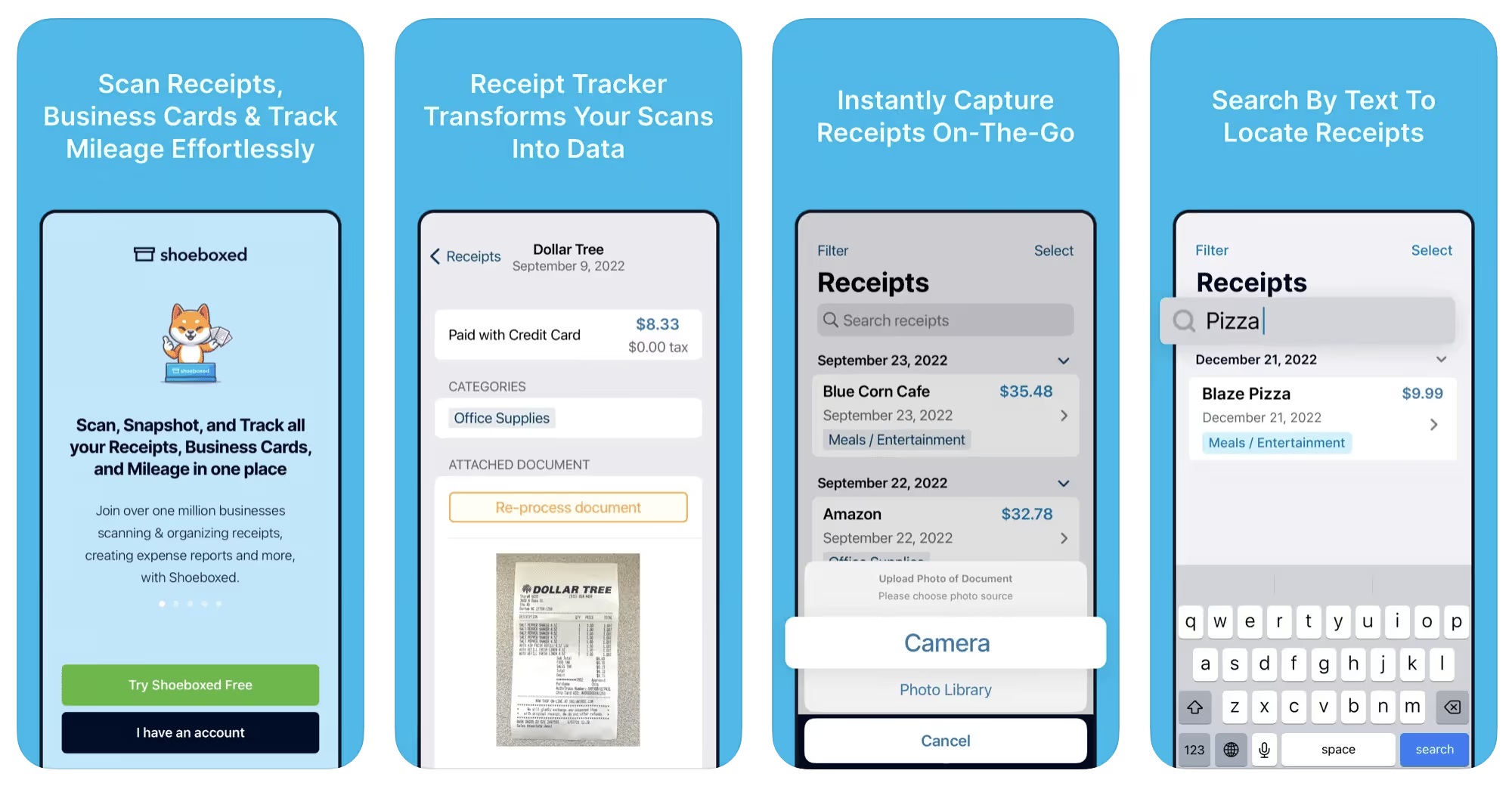

3. Shoeboxed

Shoeboxed started in 2007 as a service for scanning paper receipts into digital form. Now the app offers a free mileage tracker and has enabled users to scan receipts directly. It touts itself as the best mileage tracking app for DoorDash, but there are some elements missing that Dashers might like to have. While it provides features that record your expenses and prepare you for tax season, it doesn’t automatically track your earnings. The mileage tracker has a system where you can drop pins along your routes to make the tracking more precise, identifying those legs of a trip that you make for business purposes. The mileage tracker is “free” once you sign up for the basic version.

Available on Android and Apple: Yes

Ratings: 4.5 stars on App Store, 2.3 stars on Google Play

Free version: No

Subscription price: $18 per month for basic version

Created specifically for gig drivers: No

Source: blog.shoeboxed.com

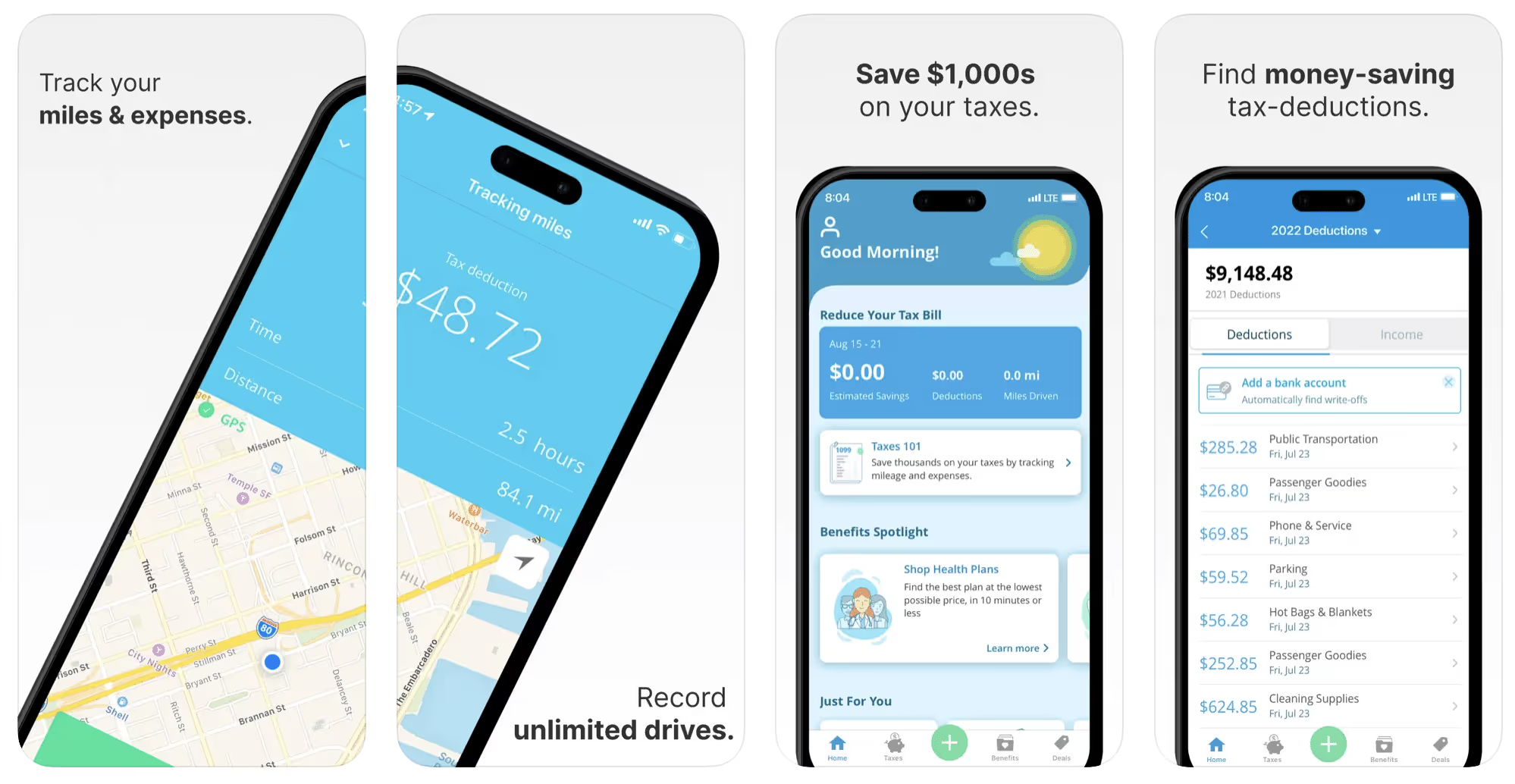

4. Stride

This free mileage tracker does a fair job of keeping track of the distances you rack up while gig driving, but it doesn’t automatically track earnings. It can be a big help, though, in tracking your expenses. You can link Stride to your bank account, and it will automatically scan your expenses to identify items you can potentially deduct. The app is totally free. This could make it the best free mileage tracker app, but there is a small price to pay. The app will persistently push you to consider various insurance plans that they are affiliated with. If you don’t mind that, this is a solid mileage tracker, even if it doesn’t track your earnings.

Available on Android and Apple: Yes

Ratings: 4.8 stars on App Store, 4.6 stars on Google Play

Free version: Yes

Subscription price: None. The app is free.

Created specifically for gig drivers: No

5. Gridwise

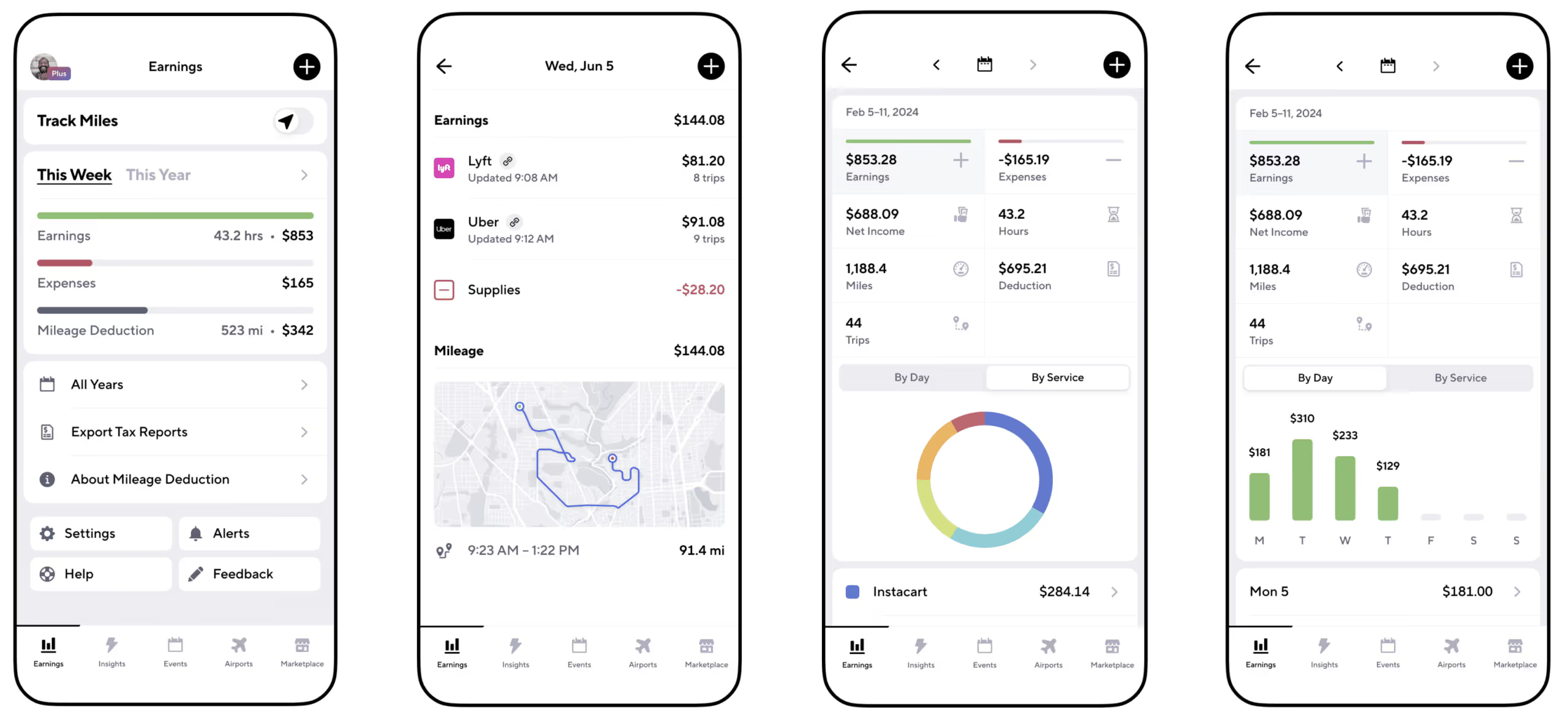

Gridwise has a free mileage tracker and free features that record your income and expenses. It gives you access to insurance and benefits, as well as insights about the best times and places to make the most money while gig driving. The Gridwise mileage tracker captures all the miles you drive while you’re on your driving shift, and it can be used if you have other trips you need to make which qualify as business travel.

Drivers love it because it is geared toward the needs of rideshare and delivery workers, providing free information about airport departures and arrivals, event start and let out times, weather, traffic, and more. The Gridwise Plus subscription adds value by providing additional insights and reports, discounts on benefits, the ability to export data in .csv format,, and more.

Available on Android and Apple: Yes

Ratings: 4.9 stars on App Store, 4.6 stars on Google Play

Free version: Yes

Subscription price: $9.95 per month for Gridwise Plus, or $95.99 per year (a $23.41 savings)

Created specifically for gig drivers: Yes!

What is the best mileage tracking app?

Now that we’ve checked them all out, we’re positive about the answer to that. Hands down, it’s Gridwise. Are we biased? You bet we are! But drivers love it too. Gridwise is the best mileage tracker app—and so much more. So many of the features are free, and the subscription to Gridwise Plus will pay for itself with additional insights to boost your earnings and deeper discounts on products and services.

Most important, Gridwise is designed specifically for gig drivers by experts who were once gig drivers themselves! Knowing what gig drivers need is a crucial step in creating an app that rideshare and delivery drivers can really use! Here are a few of the features, besides mileage tracking:

- seamless earnings tracking

- automatic, on/off toggle and manual mileage tracking

- mileage categorization

- airport, traffic, weather, and events information

- insights into where to drive and when to drive

- reports showing earnings across the platforms you use

- discounts on countless products and services for drivers

- additional resources for finding side gigs

- an informative and comprehensive blog

- affordable benefits, including insurance, medical, dental, and alternative practitioner discounts

- a community of drivers just like you

Don’t settle for just any app. Get the best mileage tracker, and so much more, from Gridwise!

[elementor-template id="21599"]

10 parking tips for drivers in big cities

When you’re in and out of your vehicle for deliveries, you want to make sure you’re leaving it somewhere safe, convenient, and legal. Unfortunately, throwing on the flashers and hoping for the best will only get you so far.

For delivery drivers in big cities, it's not always easy to find a parking spot close to your destination. If you’re not careful, you’re taking the big risk of a ticket or tow.

Plus, circling to find a spot costs you valuable time and earnings. A lot of delivery drivers also wonder if companies like UberEats will reimburse them for any parking fee or fines. We’re sorry to say the answer to that one is a pretty hard no. The same goes for courier-only services like Instacart.

But that doesn’t mean you’re on your own! Thankfully, there are a number of tactics drivers can use to ensure they have access to the best parking spots out on the road.

Here are 10 ways delivery drivers can streamline the parking process to help them save time, deliver faster, and make more money.

1. Engage your community

While not every driver is willing to risk beating the system, there are a number of different driver communities where you might be able to ask questions and gain some valuable knowledge.

For instance, Gridwise's Facebook community page brings together drivers who are interested in networking and learning how to optimize their driving business from other Gridwise users. You can also download the Gridwise app for access to exclusive driver perks and tips, and again, join our Facebook group to connect with like-minded earners.

2. Find a broken meter

We’re not going to call this a “hack,” but it’s definitely worth keeping an eye out for. If you spot a broken meter near an area you know has high traffic for deliveries, you could be in luck. Make a mental note so that you can take advantage of it next time you’re in the area.

Another way to “beat the meter” is to check what time your city makes you pay for parking. Oftentimes, there are only certain hours or days when you need to feed the meter. If you can schedule your driving around these hours, you’ll be able to save.

3. Look for curbside pickup

One of the toughest places to find parking is in densely populated urban centers. At least, that’s if you’re looking on the street. We learned from drivers that parking spots associated with your pick-up and drop-off location can be a great place to pull in. They’re usually ticketed by the hour, so if you’re quick with your delivery, you may not have to pay at all.

4. Utilize helpful apps

While navigating yet another app may not sound ideal, it can sure beat circling excessively trying to find an appropriate spot to pull over.

- Waze's “Where to Park” feature shows users available spots near their destination by calculating traffic density in certain spots.

- Way+ allows drivers the option of purchasing flexible daily and monthly parking passes that allow them to park in different spots around their city multiple times a day. Drivers who purchase a subscription can also save on gas, car washes, and auto insurance!

5. Opt into two-wheel drive

One of the best ways to eliminate the hassle of parking your car on deliveries is to well, eliminate the car. Choosing to deliver on two wheels rather than four lets you be a little more nimble and opens up more options for where you can leave your vehicle. Just be sure to bring a good lock!

6. Carry coins

The reality is sometimes your best option for making a delivery quickly is to feed the meter. With more and more city meters being converted to digital payment systems, you can save time and money by carrying enough quarters for a few minutes at the curb.

Paying $5 for a few minutes of parking in a pinch is going to cost you a lot less in the long run than taking your chances with a parking enforcement officer.

7. Scope out the area

Next time you’re out for a stroll around the block, try and take it in areas where you frequently pick up or deliver. When you know a customer is waiting, it can be difficult to take the time to look around and identify open parking spots.

This is also a great time to make note of the daily and hourly parking restrictions in certain areas.

8. Call ahead

It pays to be prepared. On any order, there’s always the chance that either the restaurant or the customer will be able to meet you at your car for a quick hand-off. While not always possible, calling ahead might end up saving you considerable time finding a parking spot.

We recommend being polite in any customer or merchant interaction. Rather than telling someone to meet you at the curb, you can try asking if there’s parking nearby or what the most convenient way to complete the delivery is.

9. Mind the curb

Colorful curbs aren’t just meant to look nice, they also serve to tell drivers where they can and can’t park. You might still remember what color indicates what, but a lot of states have unique rules that you can use to your advantage. Oftentimes, certain curb colors indicate loading zones or short-term parking that other drivers will avoid because they aren’t sure whether or not they can park there.

Here’s a guide to curb laws by state.

10. Take your time

Going along with tip #7, and as with everything in life, every once in a while it’s important to remember to just take a breath.

We know you want to make your delivery as quickly as possible to maximize your earnings, but when it comes to parking, mistakes can be costly. A parking ticket can range anywhere from $40 to $200 dollars depending on your city, easily wiping out at least an order or two if not an entire day’s earnings. While it might be tempting to try and bend the rules in a pinch, financially it just isn’t worth it.

Have a parking tip you’ve had success with? Leave a comment or share it with the Gridwise community!

The top 3 rideshare services for students and kids

The pandemic exacerbated the already problematic U.S. school bus driver shortage, revealing new avenues for the growth of transportation services for students and kids.

Some school districts have already started contracting with rideshare providers like HopSkipDrive and Zum to manage their student transit and diversify their fleet. It’s possible that transporting students through rideshare platforms could take the place of traditional school busses altogether.

And, the classroom isn’t the only destination for these drivers. Busy parents looking to skip the drive are also scheduling rideshares for their kids’ after-school events, practices and more. Drivers that work for these transportation services might also have the chance to be sitters and caregivers.

Somebody tell Ms. Frizzle to order the Uber! Today, we’re taking a magic ride through the Top 3 ridesharing apps for students and kids:

- HopSkipDrive

- Kango

- Zum

With the start of a new school year approaching, now is a great time to consider whether driving for one of these rideshare alternatives is right for you!

First, let’s clear something up.

“Uber for kids” and “Lyft for kids” do not really exist. While these rideshare alternatives for kids might take some cues from these apps, they are unique in a few key areas.

Rideshare apps for students and kids often require rides to be scheduled well in advance, rather than just hailing them on the fly.

Drivers for these transportation apps take on significantly more responsibility than rideshare drivers for adult-focused companies. The background checks and vetting process drivers go through are substantially more rigorous for rideshare apps that focus on driving students and kids.

In addition, student and child transportation services often require drivers to undergo more extensive training, obtain certifications, and in some cases, have a background as a caregiver (and sometimes function as one).

Now, let’s get into the specific differences for each of the top ridesharing apps for driving students and kids.

HopSkipDrive

HopSkipDrive’s “CareDrivers” is part of a network of rigorously vetted drivers who all have a background in childcare. Their platform is marketed toward schools and busy parents who want to set up single or recurring rides for kids.

Rather than trying to replace traditional school transit systems, HopSkipDrive wants to complement traditional routines, offering a flexible system that can accommodate off-route students and special cases.

The app has also leveraged its experienced network of drivers and heightened safety protocols to offer a rideshare alternative for vulnerable populations and older individuals during the Covid-19 pandemic.

While on the road, regular notifications are sent out to the organizer of the ride (examples being a school administrator, parent, or guardian) and HopSkipDrive’s internal support team so that everyone knows the status of the ride.

Driver Earnings

Professional CareDrivers can earn up to $50 an hour, according to HopSkipDrive! However, booking windows are usually more limited than traditional rideshare.

Payments to drivers are made every Monday via Stripe. Unlike Uber and Lyft, drivers can still get paid the entire estimated fare for canceled rides if it occurs within 1 hour of their scheduled departure time.

Credentials

Every CareDriver needs a minimum of 5 years of caregiving experience to become a driver. Other requirements include:

- At least 23 years old

- Good driving record

- 4-door vehicle less than 10 years old

- Pass multi-agency background check with fingerprinting

Some states and school districts also require HopeSkipDrive drivers to obtain advanced qualifications before getting on the road. Qualifications include CPR & First Aid, TB Risk Assessment, and district-specific training.

A primary advantage of rideshare for students and kids is the ability to accommodate students and riders that need a little extra care. CareDrivers receive support and guidance on how to provide Trauma-Informed Care (TIC) for these little riders.

Driver Feedback

HopSkipDrive shows their love for their hardworking drivers with #YourRide, highlighting the unique stories of their employees. CareDrivers aren't just earning a reliable paycheck, they're also making a significant impact on the kids. One CareDriver said:

“It’s uplifting to know I’m helping kids get to where they need to go, safely! Being a CareDriver has both financial and emotional rewards.”

Locations

HopSkipDrive serves many major cities across the U.S. Their coverage includes Northern and Southern California, The Front Range of Colorado, Virginia/D.C., Houston, Dallas/Ft. Worth, Central Arizona, Seattle, Spokane, Las Vegas, Odessa-Midland, and Milwaukee.

Kango

Kango offers rideshare services for kids of all ages with thoroughly vetted and trained caregivers/drivers.

There’s an element of connection when parents book through Kango. Drivers meet with parents before booking, and parents can request specific drivers when they schedule a ride. Drivers with Kango can also fulfill babysitting/caregiving responsibilities on request.

Recently, Kango partnered with National Express, a leading provider of student transportation services, to partner with various school districts. This move positions them to become the next iteration of student transit.

Kango stands apart from other rideshare apps for children because they are the only app insured to drive kids of all ages, and they do not have a time restriction on their childcare services.

Driver Earnings

According to their website, Kango drivers can earn up to $48 an hour during peak times. Rideshare apps for kids and students offer drivers more substantial earnings because of their increased responsibilities.

While driving windows are more limited, Kango lets drivers optimize their schedules with additional caregiving duties. Schedules are planned in advance and offer the added flexibility of working as both a driver and a sitter.

Drivers with Kango can also earn tips and choose to drive regular routes. While the earnings opportunities with Kango are great, drivers are still considered independent contractors. So, they’ll be responsible for tracking their earnings with Gridwise, and paying any necessary state and federal taxes.

Credentials

Before being approved to drive with Kango, applicants undergo a rigorous background check and must meet certain requirements:

- 3+ years of childcare experience + Trustline Certification with fingerprinting

- Background check

- DMV Check

- Vehicle inspection

- Phone screening

- Two reference checks

- In-person interview

Once all criteria are met, drivers also undergo in-person training before officially being bookable on the app.

Driver Feedback

Drivers seem to love their experience with Kango:

"I love being a part of the Kango family, especially driving the little ones around. Not only am I compensated well for my time and experience with children, but I receive the best support from the Kango team. I can interact directly with the parent within the app and can schedule my rides ahead of time. It's an app with a human touch."

Locations

Currently, Kango operates in California -- San Francisco Bay Area, Los Angeles County, San Fernando Valley, San Gabriel Valley, Orange County, and San Diego -- and Phoenix, Arizona.

Zum

Zum’s is “reimagining student transportation for safety, sustainability and reliability” according to their website. They contract directly with 4,000+ schools and districts. Unlike other student transportation apps, Zum is designed specifically for school-related transit and doesn’t offer the caregiving or parent bookings of other apps. It's becoming 21st-century school bus!

Zum offers parents and school officials more flexibility and visibility in their student transit plans. They’re also focused on creating a more sustainable model that introduces EVs (electric vehicles) to their fleet and limits the time that empty busses sit idle.

Driver Earnings

Zum states that drivers can earn up to $35 an hour and up to $750 per week.

For Zum drivers (aka Zumers), rides are scheduled by school districts base on their needs. Available rides are posted a day in advance, along with the estimated fare, and can be accepted in the driver app. That way, drivers know exactly when they’ll be driving and how much they’ll earn before they even hit the road.

Credentials

Zum offers two options for schools: traditional and non-traditional student transportation.

Regardless of what type of driver you are, every Zumer must:

- Be at least 21 years old

- Preferably have some childcare experience

- Complete a comprehensive interview process

- Possess a clean driving record

- Pass thorough background checks

- Complete all state and company training and maintain valid licensing

Traditional drivers must also pass driver qualifications and obtain a commercial driver’s license with endorsements. Non-traditional drivers need a car that is fewer than 10 years old and able to pass regular inspections.

Locations

Zum operates in major U.S. markets including: The Bay Area, Los Angeles, Chicago, Dallas, and Seattle.

Their innovative approach to student transportation services is enabling them to expand rapidly. Potential coming service areas include: Orange County, Phoenix, Portland, Sacramento, D.C., New York City, San Diego, and Miami.

Local tribute: Zemcar

Currently only operating in the Greater Boston area, Zemcar was a little too small to make our list this time around. But they’re still a great rideshare alternative for kids and students. If you’re in the area, consider signing up today. Or, keep an eye out for them as they expand their market.

What’s fueling the move from traditional student transportation?

Rideshare transportation services for students and kids offer a flexible alternative to the headache of managing a bus fleet. These apps provide parents and schools with custom solutions to safely get kids where they need to be. Smaller vehicles like sedans can pick up off-route students while larger busses drive the main routes.

The Every Student Succeeds Act passed in 2015 put a renewed focus on providing better access to educational opportunities for youth in foster care, unhoused students, and students with special needs. The law mandated that districts provide transit for these students to their school of origin even if they moved out of the district; a regulation that is far easier to implement with rideshare than bus transit.

Thinking About a Change?

If you're looking for more rewarding work, consider signing up for one of these transportation services. But, keep in mind that getting appointed as a driver will take time.

If you’re ready to make the leap but worried about the financial implications, you might want to consider a personal loan through our partner, Giggle Finance. These extra funds can give you the cushion you need to jump in and start helping the kids and supporting the community!

All drivers save with Gridwise!

Gridwise offers all rideshare and delivery drivers new ways to save. Automatically track your mileage and log your expenses effortlessly in the app to make tax time a breeze. All of your data is collected and turned into simple, elegant graphs, (shown below), to help you analyze and maximize your earnings.

Join our community and become a Gridwise user to gain access to great driver perks like Gridwise Gas and Gridwise Connect! And if you're not convinced yet, take a look at what our users are saying. Keep more of what you earn, start by Downloading Gridwise today!

Delivering on two-wheels: how to make money without a car

Grab your bike, scooter, or running shoes because, believe it or not, you can make money delivering without a car! Although, it might seem like you’re missing something extremely fundamental, most grocery, food, and package delivery apps allow you to deliver on a bicycle, scooter, or motorcycle in select areas. Even if you own a car, there are instances when delivering on a two-wheeler might make sense.

If you’re still unsure about this, we further breakdown the advantages and disadvantages of delivering on two-wheels rather than a car.

Advantages of delivering on two-wheels

- Low entry cost: A bicycle or a scooter costs significantly less than a car, making them a better option for those who are looking to get into gig work. If you are already delivery driving but you’re looking for more ways to save, buying a bicycle or scooter is an economical way to test the waters.

- Low operating costs: The operating costs of two-wheelers are also significantly less than that of a car. Significantly lower insurance costs, less maintenance, and virtually no fuel costs (depending on if riding on a bicycle or motorized scooter) add up to substantial savings.

- Low financial pressure: Eliminating the worries about paying a vehicle loan at the end of every month can help make your work life a little less stressful and more enjoyable.

- Navigate through traffic: During peak delivery hours, navigating through traffic (for instance riding in the bike lane) has a tremendous impact on your earnings.

- Parking: Finding a parking spot for your car can be very challenging in urban areas, often forcing you to park your vehicle far away and having to walk a long distance to the destination.

- No license requirements: If you don’t have a driver’s license, then opting for two-wheel delivery can expedite the process of getting you on the road to make more money.

- Health benefits: Get paid to get fit! Not only are you saving on gas and other expenses, but you can also skip the pricey gym membership and get paid to exercise when you opt for a bike over a car.

Disadvantages of delivering without a car

- Not a rainy day option: Two-wheeler vehicles are not feasible when you want to operate in an area that sees frequent and extreme weather changes. Rain, snow, or a hot summer can all drastically impact your earnings if it means you won’t be able to complete deliveries in these weather conditions.

- Less cargo space: The bigger the order, the bigger the payout. Delivering on a bike, scooter or motorcycle limits the amount of “cargo” you can carry due to the lack of storage space. With a vehicle, you could potentially deliver a feast to a family reunion!

- Longer wait times: There will be days where you are filled with uncertainty. Sometimes, you may get back-to-back orders, while on the other hand, you may experience a longer wait period in between orders. Being able to wait in your car, and possibly switch over to ridesharing, is an advantage on days when delivery orders are slower.

- Cannot rest between orders: When you travel long distances or in areas with heavy traffic, it can wear you out. Having a car makes it easy to rest between your orders or in the middle of a long shift.

- The order payout may be low: Delivery apps take your vehicle, order size, distance, and other factors into consideration while sending you orders. If you are riding a two-wheeler for delivery, like a bicycle, you are more likely to receive smaller, short-distance orders that generally pay less per job.

- Limited driving and earning options: Having a car opens up more avenues to make money by allowing you to combine rideshare and delivery opportunities.

- Health risks: Riding a bicycle for an hour or two every day may have some health benefits, but doing the same for hours together every day in traffic and pollution might harm your health in the long run. It’s also important to understand the risk of injuries from accidents is also higher when riding a bicycle, scooter, or motorcycle.

What are the best companies for carless drivers to work for?

Here are some of the bigger companies that allow delivery without a car:

- UberEats – UberEats allows drivers to deliver on a bicycle, scooter, motorcycle or by foot. Check their website for information specific to your city. Since Uber acquired Postmates last year, the same policy applies to deliveries on the Postmates app.

- DoorDash – DoorDash has a similar policy to Uber Eats and allows deliveries on bicycles, scooters, motorcycles, or foot.

- Instacart – Instacart doesn’t explicitly limit drivers from using a two-wheeler for deliveries. However, since it is primarily focused on grocery delivery, the order size might be too big to deliver on a bicycle or scooter. Though delivery “riders” can pick and choose smaller orders, they are less common and result in lower payouts.

Don’t sleep on local delivery companies like Favor! Newer companies usually offer incentives to quickly attract more drivers to their platform and expand their business, and what’s better than supporting a local business?

What are some local delivery companies in your area? Let us know on our community Facebook page!

Should you deliver without a car?

Absolutely. Most platforms allow delivery on bicycles, scooters, and other transportation types. Rather than paying off expensive monthly loans, trying out a two-wheeler for your driving gig might be a better option financially. Even if you are an experienced delivery driver, there are instances when delivering on a bicycle or a scooter can be more convenient and economical for your business.

As a car-less driver, it’s still possible to make as much money as someone with a car. However, this largely depends on your location and the geography of your delivery zones. Generally, transportation on two wheels is more suitable for urban centers where it is more congested with people and cars. Again, this alternative option will keep your costs low and help you deliver more orders during peak hours by quickly moving through traffic.

Whatever you drive, drive with Gridwise!

Scroll through our blog for tips and tricks on how to boost your earnings and make the most out of your time on the road! Gridwise can help you make money, save money and optimize your driving strategy.

Gridwise can help you keep track of your performance, earnings, mileage, and so much more across your delivery and rideshare platforms. Gridwise also offers reliable weather alerts, event updates, and hotspot alerts, so you can strategize when and where you should drive.

Download the app, sign up for a free Gridwise account, link all of your rideshare and/or delivery accounts and then see how Gridwise can help fatten up your wallet!

The best navigation apps for gig drivers

Rideshare and delivery drivers depend on navigation apps to accurately and efficiently get where they need to be. An app that glitches or neglects to alert drivers about traffic jams and construction delays can cost time and money.

In this post, we provide an overview of the most popular navigation apps. We also rate them according to how well they support gig drivers. Here’s what we outline:

- The bare necessities of navigation systems

- The Big Four: Google Maps, Uber Navigation, Waze and Apple Maps

- How to sync external navigation apps

The bare necessities of navigation systems

The many features of navigation apps can provide convenience and a sense of simplicity, but the two essentials for rideshare and delivery drivers are accuracy and reliability. If you’re unsure about where to go to pick up a passenger or where to drop off a delivery, you can’t afford to waste time with a GPS that doesn’t know the best and most efficient routes.

For instance, if your navigation app gives you driving directions that send you to the back alley instead of the front door, or to First Avenue instead of First Street, you could face a lost ride or delayed delivery. To do your job well, you need accurate and reliable turn-by-turn instructions to depend on.

A good navigation app should constantly provide you with directions, no matter what happens to your signal. Whether you’re in a congested urban environment or out in a rural location, you need an app that can reliably keep your route straight.

These are the bare necessities for any decent navigation app, so you might be surprised to discover that not all of them deliver. Keep these requirements (and your individual needs) in mind as you consider the best navigation app for you.

The Big Four

There are four major navigation apps that rideshare and delivery drivers use. While Uber has its own navigation system called Uber Navigation, Lyft’s navigation app uses one of the most familiar and widely used navigation systems, Google Maps. Waze is also part of the Big Four listed here but has a separate identity from Google Maps after being purchased by Google in 2013. Another common app that drivers use is Apple Maps, but this is only available to Apple iPhone users.

These apps have an array of features that can also apply to personal driving and other ways of getting around, such as walking and public transportation. Here, we will focus on the apps and their utility for rideshare and delivery driving.

Now, let's breakdown each app so you can decide which navigation app works best for you.

Google Maps

Google Maps is the most trusted and widely used navigation app in the world. It’s built into many driving platforms and has a variety of features that help drivers find their way around.

Why you’ll like it:

- As the gold standard in navigation, Google Maps has everything rideshare and delivery drivers need. It’s comprehensive and provides turn-by-turn directions.

- The standout feature for Google Maps is that it provides directions for drivers on which lane they should be in when they exit a highway. Other apps may not have this feature, leaving you to guess when it comes to making quick exits from overcrowded freeways and parkways.

- You can also use the “My Location Now” feature to see where you are on the map. To get to your exact location, tap the arrow in the lower right corner of the Google Maps screen, and the map will hover to your location.

- Google Maps also allows you to download maps so you can use them offline. This feature could keep you from getting lost the next time you retrieve hikers from a remote trailhead with no cell service.

The downside:

- There are ads. Despite its high-tech demeanor, Google is, in essence, an advertising company. It should be no surprise that ads are placed throughout the app and can potentially distract you from getting a good view of where you’re going.

The images below show you the best and less favorable features of Google Maps. The first screenshot is the standard view, while the screenshot on the bottom is Google Maps street view, which gives a more detailed depiction of the streets and what structures are on them. You can also see the icons that reveal an array of local Google Maps advertisers when tapped on the screen. So, despite the cluttered screen, it’s hard to complain about the comprehensive features and reliability.

Uber Navigation

Uber Navigation is a built-in feature for Uber and Uber Eats drivers. Not previously known for its slick appearance or its reliability, Uber has recently instituted some upgrades.

Why you’ll like it:

- Working with Uber Navigation makes driving and navigation seamless. You don’t have to worry about switching back and forth from your driving app to an external navigation app.

- Recently, Uber Navigation has upgraded its maps and graphics to make it easier for drivers to see exactly where they’re going.

- For passenger pickups, you can now see which side of the street passengers will be on. This update might not sound like it would have an impact on drivers, but in congested areas, this feature can be extremely helpful. For instance, there may be more details regarding the pickup spot, such as the name of a business, rather than just a street address.

- Drivers can choose up to three different routes to get to each destination, depending on their preferences. These options could allow you to avoid tolls, construction areas, and roads that can be difficult to drive on.

- Uber has also improved its navigation app to incorporate traffic conditions into its calculations of the best routes to take.

- Plus... at least for now, there are no ads on the map.

The downside:

- You can only use Uber Nav while driving for Uber or Uber Eats. If you multi-app, switching from one navigation app to another can be an adjustment you might not want to deal with.

- As the image below shows, Uber Navigation’s look is still far from sexy and lacks the detail shown on other apps. This particular shot shows the option to take alternate routes. While some might find this useful, drivers in a hurry want to know one thing: what is the fastest route?

Waze

This funky, yet functional, navigation app is popular for a few reasons. Waze was acquired by Google in 2013, giving it superior reliability and formidable mapping power. However, it’s remained a stand-alone navigation app due to its unique nature.

Why you’ll like it:

- The Waze app’s information is crowd-sourced, so you get current data from other drivers about traffic, road hazards, and where police have been seen.

- Waze has the same features as Google Maps, including the ability to save directions offline.

- You can customize the navigation voice to a variety of accents and characters. The most recent is Master Chief from the Halo universe. (You can also mute the nav voice if need be).

- Waze interfaces with most major driving and delivery platforms. You can change your settings to make sure it’s active on your app.

- The Waze map is clear and easy to follow, as you can see in the image here:

- Waze directions will provide you with the best route to avoid traffic problems and weather-related hazards. It offers three different routes, if available, which you can view with one tap of the screen.

- You can integrate your music, podcast, and audiobooks apps with ease. You can even set it to pause the sound when you’re using audio for Waze directions.

The downside:

- The screen can get cluttered with icons like your music app, reports, notices about railroad crossings, and alerts about vehicles stopped on the road.

- There are ads, TONS of them. Worse, they pop up at the top of the screen, right where the directional arrows and street names appear.

- Waze takes up a lot of battery, and a big chunk out of your data allotment. If you keep your phone on a charger, you’ll solve the first issue, but unless you have an unlimited data plan, you might have some problems utilizing Waze.

Apple Maps

Like all things Apple, the design is slick and it works without a glitch... most of the time. It is reliable and uses traffic information from Tom Tom, which is a long-established navigation company. If you use an iPhone, you have Apple Maps included as one of your phone’s default apps.

Why you’ll like it:

- Apple Maps is integrated with Siri. When you’re truly lost, just ask Siri to take you to an address or point of interest. Apple Maps will open and guide you there.

- Apple Maps street view is easy on the eye. It’s hard to see any flaws in the appearance of Apple Maps, as you can see in this screenshot below:

The downside:

- Apple Maps is not always reliable, especially when it comes to finding the fastest route between Points A and B.

- Apple Maps is available only to iPhone users.

- Apple Maps does not integrate with major driving apps. Meaning, that if you use it, you’ll have to work in tandem with the driving app while you navigate to your pickup point or destination.

How to sync external navigation apps

Once you choose the navigation app that works best for you, it’s easy to arrange it so your gig driving app will automatically transition to the external navigation app while you’re working. You will need to check within your app to see if there are instructions specific to your platform, but for the most part, here’s how it works:

- Open your driving or delivery app.

- Go to App settings

- Tap “Navigation”

Here you will see your options. Your app will permit you to select its proprietary app (Uber Navigation or Lyft), Google Maps, Waze or Apple Maps (for iPhone users).

Select the app of your choice, and if you can, tap on the option that allows it to automatically go to your favorite navigation app as soon as you accept a ride or delivery request.

Now, you can drive using the navigation app that works best for you!

Gridwise: Your go-to app for tracking earnings, driving insights and more

All the best navigation apps will get you where you’re going, but Gridwise lets you make more money along the way.

Optimize your driving strategy with information about passenger volume at airports and local events, weather and traffic alerts, and the ability to track your earnings and expenses. With a few taps, a snapshot of your gig life will appear on this slick, easy-to-read screen:

Watch your business grow with in-app perks, offered exclusively to Gridwise drivers.

Want to make better decisions about your driving strategy? Start earning up to 39% more with Gridwise. Download the app today!

Becoming a DoorDash Top Dasher: Is it worth it for drivers

DoorDash has become one of the largest online food ordering and delivery platforms in the United States. By the end of last year, they racked up over 450,000 merchants, 20 million customers, and a million delivery drivers, also known as “Dashers.”

DoorDash is a reliable platform for delivery drivers to earn a part or full-time income. If you are willing to put yourself to work, it's possible to make $1000 a week with DoorDash, especially if you strategize and use the right tools.

But today, there are over one million Dashers on the platform, creating a lot of competition among drivers trying to win orders. To maximize earnings, drivers need a better way to stand out and get more deliveries.

If you’re looking to improve your Dasher game, you might consider becoming a Top Dasher. Here’s what you need to know about the program:

- What is the Top Dasher program?

- What are the benefits of becoming a Top Dasher?

- Are the benefits worth the effort?

- When does it make sense to be a Top Dasher?

What is the Top Dasher program?

The Top Dasher program is a rewards program that recognizes and rewards high-performing delivery drivers. These drivers have high customer ratings, acceptance ratings, and a high percentage of successful deliveries.

If you want to reach this pinnacle in food delivery, here’s what you need to lock down each month.

1. A stellar 4.7 customer rating

2. Minimum 70% order acceptance rate

3. At least 95% delivery completion rate

4. Over 100 completed deliveries in the month

5. Have 200 completed lifetime deliveries as a Dasher

This program is intended to motivate Dashers to accept and complete as many deliveries as possible. While such performance from drivers is hugely beneficial for DoorDash, whether it’s rewarding for drivers is worth asking. Before we answer that, let’s take a look at the benefits DoorDash offers to drivers that qualify.

What are the benefits of becoming a Top Dasher?

The Top Dasher program is a monthly program that renews on the first day of each month. If you meet the Top Dasher criteria by the end of the current month, you get access to benefits for the following month.

There are two primary reasons you might consider becoming a Top Dasher: more deliveries and to "Dash Anytime."

More deliveries

DoorDash’s system gives preferential treatment to Top Dashers over regular drivers when both compete for the same order. For example, if there are two Dashers nearby and someone searches “pizza delivery near me,” the system gives the Top Dasher the option to take the order first. This can help you beat the crowds and earn more on deliveries, even in crowded markets.

Lately, DoorDash seems to be tweaking this benefit in some cities. Rather than prioritizing Top Dashers for all orders, the company is experimenting with giving priority access for high-value orders (orders above $30). These tweaks could be DoorDash's move to address one of the biggest complaints they receive about the Top Dasher program – Dash Anytime.

Dash Anytime

Any driver can dash and compete for orders without scheduling in advance. When a zone is busy it is marked red on the driver map. However, when order volume is low in a zone, (marked grey on the map), DoorDash places restrictions on who can dash. This balances supply and demand and ideally gives drivers better opportunities to earn without having to wait too long between orders.

Top Dashers are exempt from this restriction and can dash anytime, anywhere, without prior scheduling. But, the option to dash anytime doesn’t guarantee orders. If things are slow in a zone and there are multiple Top Dashers online, drivers will face the same competition for orders that they usually would compete for without being a Top Dasher.

If you have questions about the Top Dasher program or want to check your status, you can contact DoorDash support for drivers. More information on how to contact DoorDash support can be found in this article!

Are the benefits worth the effort?

Now, the million-dollar question is: Are Top Dasher benefits worth the effort? Unfortunately, the answer is not straightforward and can vary from driver to driver and city to city. While becoming a Top Dasher is generally a good thing, there are certain factors that you need to consider while evaluating the program and its impact on your earnings.

You may have to accept more low-value orders

This is the most apparent disadvantage of the Top Dasher Program. With the requirement to accept at least 70% of the orders offered, drivers are forced to take many low-value orders and might miss out on higher-earning opportunities.

When a Dasher has to drive more than 20 miles round-trip for a payout of less than $5, it doesn’t make financial sense to accept the order. A Dasher would likely refuse these orders if they weren’t planning to become a Top Dasher.

However, reaching or maintaining a 70% order acceptance rate is possible even while refusing low-value orders. Since the target needs to be reached by the end of the month, drivers can strategize by being selective at the beginning of the month and changing course towards the end if they fall short of the goal.

The Dash Anytime dilemma

Some drivers would argue that the option to dash anytime without scheduling isn't much of a benefit and does not translate into substantial earnings. However, DoorDash explicitly recommends that Top Dashers should continue to schedule slots and dash in busy areas.

When does it make sense to be a Top Dasher?

Being a Top Dasher is not a one-size-fits-all approach to higher earnings.

It’s a beneficial program if you want to schedule to dash in advance and want the flexibility to work when and where you want to. It’s also helpful if you switch zones frequently.

But, if qualifying for the program means accepting too many low-value orders in your zone, it may not be worth the time and effort. You’re better off focusing on scheduling time in advance and accepting more big-ticket orders to maximize the value of your time. If you happen to meet the criteria for Top Dasher while doing that, well, that’s just an added bonus.

You don’t have to be a Top Dasher to earn more with Gridwise!

Deciding what works for you as a Dasher takes time. Questions like when and where to dash, and which orders to accept require insights you won’t find in the DoorDash app… but you can find them in the Gridwise app!

Gridwise helps you track your performance and earnings across rideshare and delivery platforms to understand what strategy is working best for you. Your data is automatically collected and beautifully displayed (see above).

Features that show you the best times to drive, weather alerts, event alerts, real-time flight alerts, and custom airport alerts offer you new ways to optimize your driving strategy and earn more as a driver.

You can also access more ways to grow your business, like exclusive driver perks right in the app.

Download the app today and see how Gridwise can help you make smarter decisions about your driving. Start earning up to 39% more with Gridwise!

Insurance for independent contractors: what to look for and how to get it

Finding or getting complicated things such as TLC compliant insurance doesn’t sound quick or easy, but if you know what you’re doing, it can be both. In this post, we’ll share what we know, including the key steps toward getting what you need, including:

- Why drivers need extra insurance

- The types of insurance available

- What to look for in an insurance policy

- Insurance for rideshare drivers

- Inshur: quick, easy and protective TLC insurance for rideshare drivers

Why drivers need extra insurance

When you’re a rideshare driver, your personal auto policy won’t cover everything. Uber, Lyft or Via may provide additional coverage while you’re picking up or carrying passengers, but that’s still not enough. All drivers, everywhere, need to have rideshare insurance simply because they’re using their vehicles for commercial purposes.

You shouldn’t try to ignore or get around this when you’re a rideshare driver. If you’re not protected, you could wind up in a lot of trouble. For instance, if you don’t bother to tell your insurance carrier that you’re a rideshare driver, they could refuse to cover you, even if you file a claim for an incident that happens while you’re totally off the app.

In some localities, such as the New York metropolitan area, there’s even more to consider. To drive for a rideshare company in New York City, drivers must meet the requirements of the Taxi and Limousine Commission (TLC). They are legally required to have a TLC license, TLC plates, and TLC insurance.

As you can see, there can be more to insurance for rideshare drivers than meets the eye. Let’s look more closely at rideshare driver insurance coverage to see what you really need.

What kinds of insurance are available?

There are two basic kinds of insurance. First, there’s the auto liability coverage policy. In most states, it’s not possible to legally drive at all, let alone for rideshare, unless you carry a basic liability policy. Most Uber and Lyft drivers purchase a rideshare endorsement as an add-on to their basic policy.

As we pointed out above, rideshare drivers who work in New York City need the second kind of policy, which is TLC insurance. This policy protects third parties, namely passengers and other drivers. TLC insurance does not cover injury or damage to you or your property, so you will need additional coverage for yourself.

How can you get the most coverage for the least amount of money? That’s always a great question. Let’s start by learning more about what insurance policies have to offer.

What to look for in an insurance policy

There are basic requirements for drivers in every state, and you can learn more about them from your local insurance companies and agents. Your lender might also give you additional requirements for insurance, in many cases. You’ll need to check into all that, but in general, you will need policy that has at least these types of coverage:

- Liability: covers bodily injury and property damage to another person or their property.

- Uninsured and underinsured motorist coverage: protects you from being stuck with medical and/or repair bills should the other party involved be without adequate coverage of their own.

- Comprehensive coverage: covers damage resulting from theft, fire, weather, or vandalism.

- Collision: allows you to get money to repair or replace your car should you hit another vehicle or an object that damages your vehicle.

- Medical payments: pays for hospital visits, surgery, X-rays and other medical costs resulting from an accident.

- Personal Injury Protection: This kind of coverage isn’t available in all states. It pays for medical expenses, but also may help to cover your costs for child care or lost income.

- Optional protection might include coverage for rental reimbursement, transportation expenses, gap insurance, towing and labor costs, sound systems, and rideshare.

It’s also good to have flexibility, the option to choose the types of coverage, beyond what’s required, that you wish to purchase. In addition, it’s crucial to determine whether your policy’s coverage has limits that are per person or per accident. Also keep your eyes peeled for the costs of deductibles. If you make a claim, you won’t want to have to pay more than you can afford before the insurance even kicks in.

As you can see, there’s a lot that goes into knowing what the right policy for you might be. Don’t buy until you feel comfortable with what you’re getting. Always purchase insurance from a company you can trust to give you the most coverage for a fair amount of money.

Insurance for rideshare drivers

One of the first things you should look at when you buy insurance is whether the company you’re dealing with has policies designed for rideshare drivers. Rideshare insurance in New York is a special case, and the company you choose should have expertise in these two types of coverage:

TLC Insurance:

If you want to be a rideshare driver in New York City, TLC Insurance isn’t optional. The TLC regulates the activities of all activities related to customers who pay to be driven from one place to another by a driver or company. Because of the mandatory nature of TLC Insurance for independent contractors, you won’t be cleared by any rideshare app without it.

TLC Insurance requirements are put into place in order to protect passengers, pedestrians, and other drivers who may be affected by a mishap caused by a driver for hire. Based on your vehicle and the number of passengers it holds, coverage may vary, but the baseline minimum coverage is as follows:

- $100,000 per person

- $300,000 per accident

- $200,000 personal injury protection